Every scaling technology company eventually reaches an infrastructure inflection point. In the early stages, public cloud is the obvious choice: speed, flexibility, and elasticity matter more than cost. As workloads mature, however, the economics shift. Demand becomes predictable, cloud spend accelerates, and infrastructure ownership begins to look increasingly attractive.

This article explores where that transition occurs, why it matters, and how organizations can recognize when they’ve reached it.

Co-authored by Yuriy Shyyan and Sash Ghosh

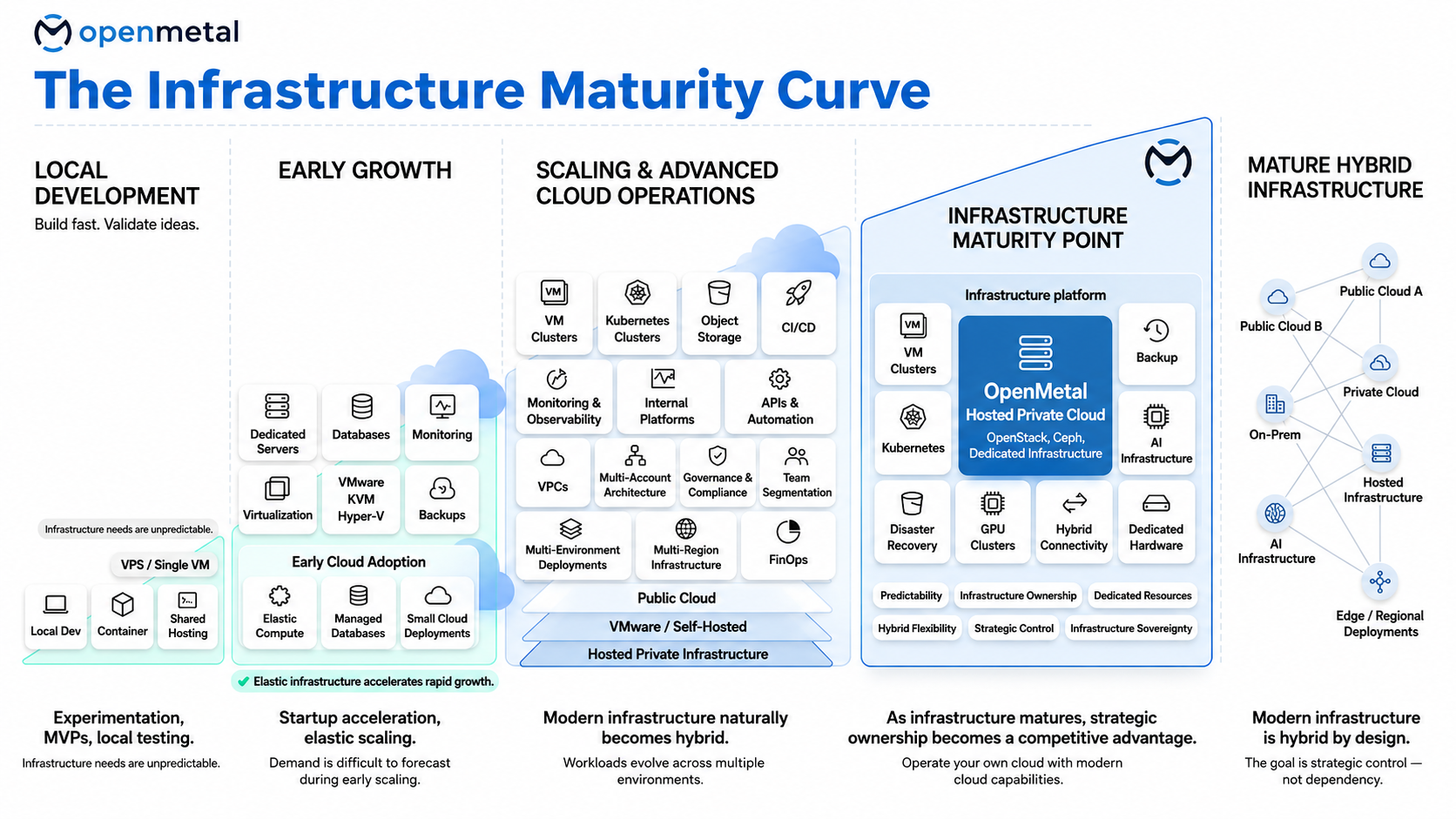

The five stages of infrastructure maturity

Every scaling technology organization moves through a recognizable progression. The labels vary by company and industry, but the underlying shape does not.

Key Takeaways

- Public cloud is usually the correct choice during early growth.

- Infrastructure economics change as workloads become predictable.

- Most organizations reach an inflection point between scaling and mature operations.

- Hybrid infrastructure is the end state for many successful companies.

- The question is not whether to use public cloud, but where ownership creates strategic advantage.

Stage 1 — Local Development

DIY over costly infra decisions. Zero to minimal spend.

Example: A SaaS startup running a handful of containers and a shared database.

Builders are experimenting. Workloads are unpredictable, requirements change weekly, and the right answer is whatever lets the team validate ideas fastest. Local environments, containers, shared hosting, single VMs. Infrastructure cost is in the noise of the budget. It is not yet a strategic concern.

Stage 2 — Early Growth

Elastic scaling earns its premium. Optionality is the real product.

Example: A venture-backed company rapidly scaling customer acquisition on AWS.

The product has traction. Demand is difficult to forecast, and elastic infrastructure earns its premium: pay as you grow, scale as needed, do not overcommit on capacity that may not be used. The per-unit cost is high, but the absolute number is still small, and the option value of elasticity is real.

This is the stage where most organizations fall in love with the public cloud, and rightly so.

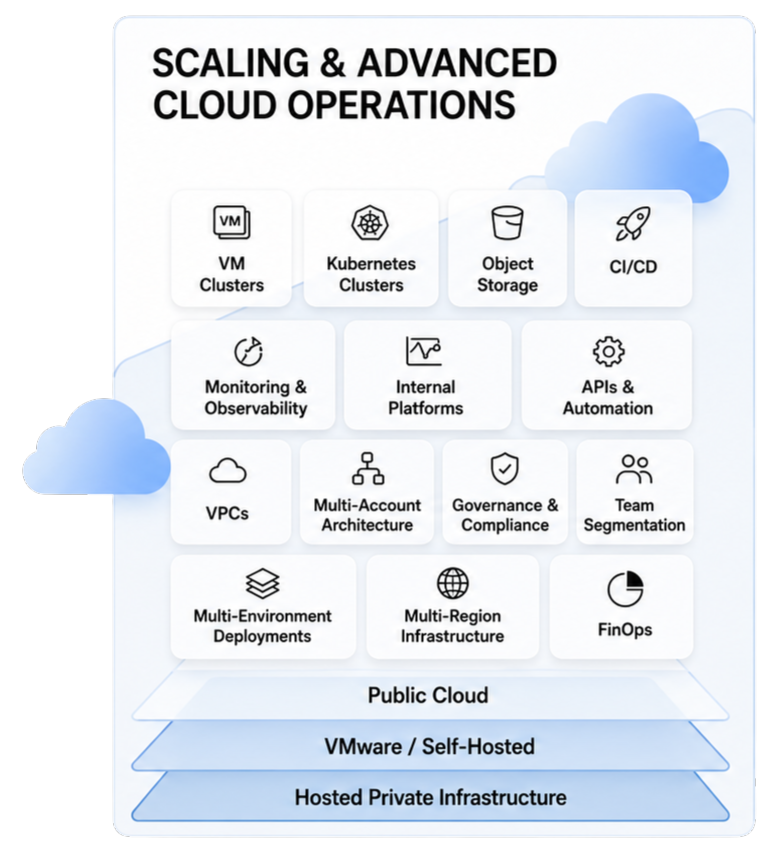

Stage 3 — Scaling and Advanced Cloud Operations

Cloud bills grow faster than workloads. FinOps becomes standard practice.

Example: A company operating Kubernetes clusters across multiple environments with a growing FinOps practice.

Footprints expand. Internal platforms emerge. Workloads are no longer monolithic; they live across VM clusters, Kubernetes, multi-account architectures, and increasingly stringent governance frameworks.

This is also the stage where the cost conversation changes. The cloud bill stops looking like a tax on growth and starts looking like a line item growing faster than revenue. FinOps teams form. Cost-driven design reviews become standard. Hybrid emerges, in part, as a cost-optimization play.

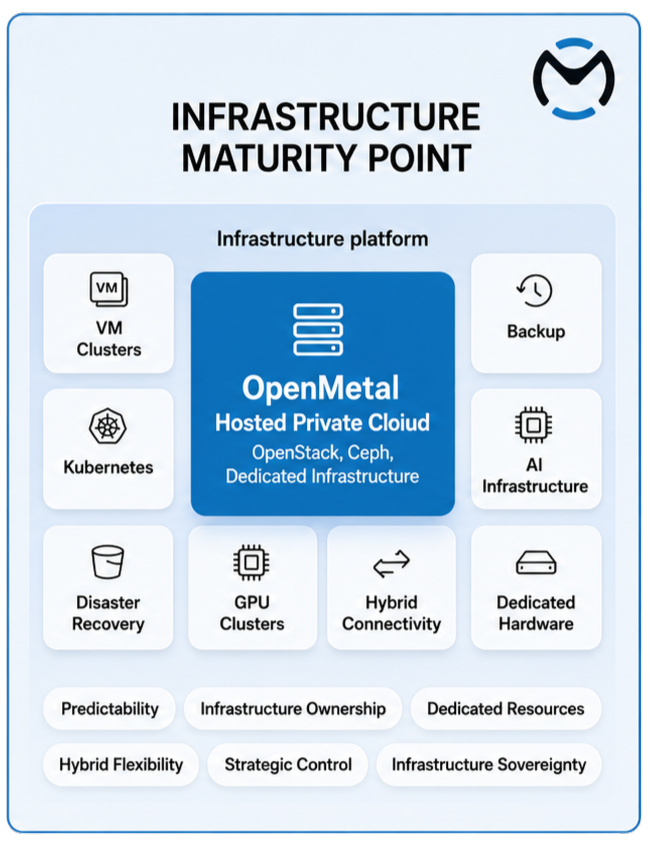

Stage 4 — Infrastructure Maturity Point

Ownership begins to outperform rental. The math reverses.

Example: A business spending hundreds of thousands annually on cloud infrastructure with predictable workload patterns.

Workloads are stable. Demand is predictable enough to size for. The technical capability to operate cloud infrastructure exists in-house.

At this point the constraint shifts. The question is no longer “how do we scale fast?” but “what are we paying for capacity we could own?” This is the inflection point where ownership begins to outperform rental, not in some workloads, but in the steady-state economics of the whole portfolio.

Stage 5 — Mature Hybrid Infrastructure

Hybrid by design. Cost structure is intentional, not inherited.

Example: A mature organization deliberately placing workloads across public cloud, private cloud, AI infrastructure, and edge locations.

Infrastructure is portfolio-managed. Public cloud, private cloud, on-premises, hosted private infrastructure, edge, AI workloads — each is deployed where its cost, performance, and operational profile makes the most sense.

Hybrid is by design, not by accident. The cost structure is intentional rather than inherited.

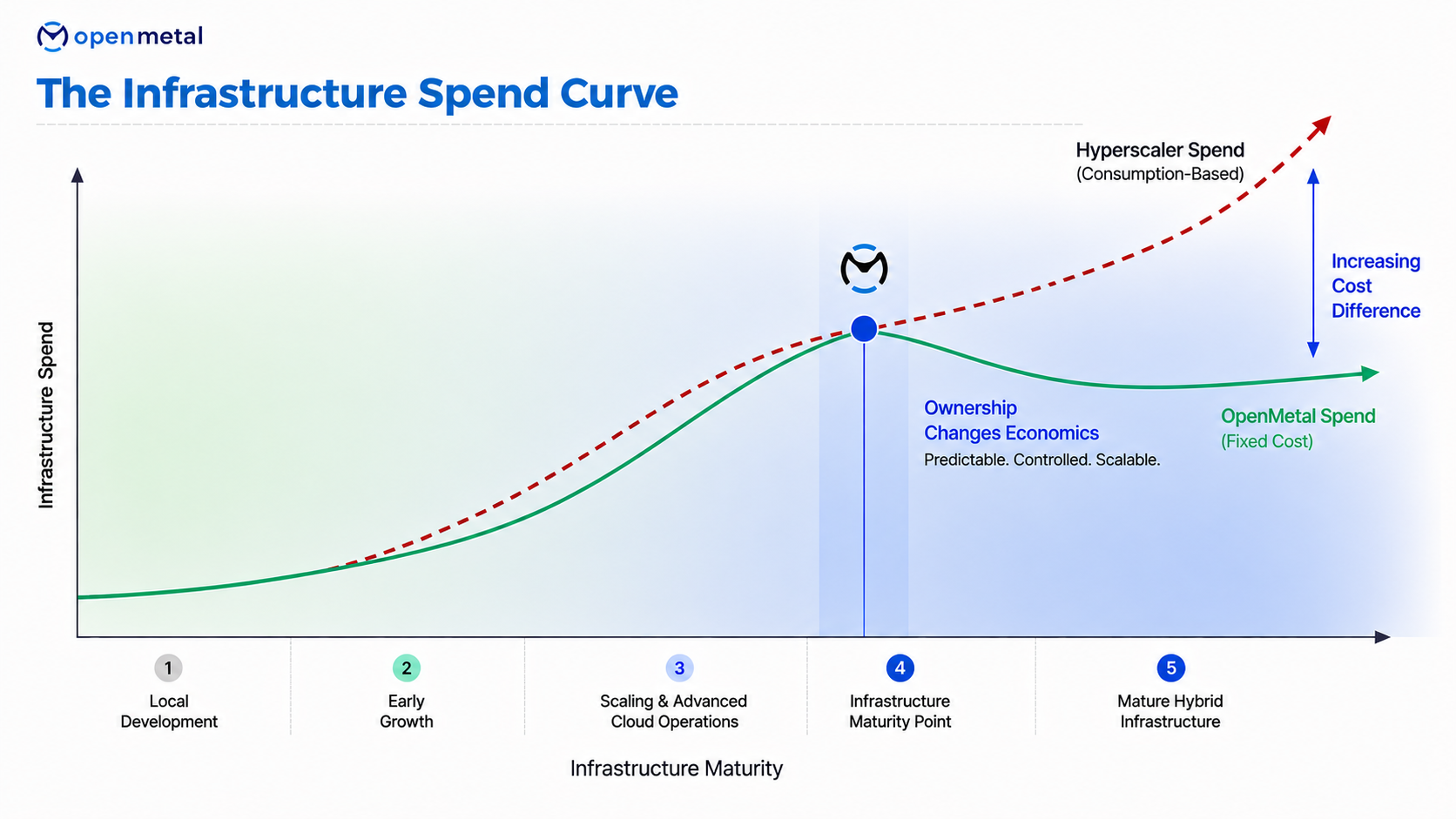

The spend curve: where the economics reverse

The maturity curve explains how organizations evolve. The next question is what happens to infrastructure economics as they move through those stages. That’s where the spend curve becomes important.

Critically, the two consumption models implied by the maturity curve do not scale the same way.

Consumption-based hyperscaler spend (the dashed curve) is brilliant when demand is unpredictable. Every dollar tracks usage, and the model is built for elasticity. The organization pays for that elasticity in two ways: a per-unit premium on compute, storage, and egress, and the operational simplicity of not owning infrastructure. Below a certain utilization threshold, this is the right answer.

Capacity-based ownership (the solid curve) is the opposite shape. Cost is paid up front, or amortized through hosted private infrastructure. The per-unit cost is low. The trade-off is operational ownership and the need to size capacity intelligently. Below a certain utilization threshold the model is uneconomic. Above it, the math reverses.

The critical insight is that these curves cross. There is a point where ownership becomes cheaper and stays cheaper, and the gap does not stop growing. Past the crossover, every additional unit of consumption widens the difference between the two models.

For most organizations, that crossover sits somewhere between Stage 3 and Stage 4. It is not defined by company size, revenue, or headcount. It is defined by three things: infrastructure utilization, demand predictability, and the in-house capability to operate cloud-native systems on owned hardware.

What the Spend Curve Is — and Isn’t — Telling You

The spend curve can be misunderstood as an argument against public cloud. It is not.

The chart does not suggest that infrastructure ownership is always cheaper. It does not suggest that every workload belongs on private infrastructure. And it certainly does not suggest abandoning public cloud altogether. In fact, for organizations in the early stages of growth, the opposite is often true. When demand is unpredictable, elasticity is worth paying for. Public cloud remains one of the most effective tools ever created for turning infrastructure into an on-demand service.

What the spend curve illustrates is something more specific: infrastructure economics change as organizations mature.

As workloads become more stable, utilization becomes more predictable, and operational capabilities mature, the premium paid for elasticity begins to exceed the value received from it. The economics shift from optimizing for flexibility to optimizing for efficiency. That is why the two curves eventually cross.

The Infrastructure Maturity Curve explains when organizations typically reach that point. The Infrastructure Spend Curve explains why the economics begin to favor a different model.

The key takeaway is not that one infrastructure model is universally better than the other. It is that different stages of organizational maturity benefit from different infrastructure models. The most successful organizations understand where they are on that journey and intentionally deploy each workload where it creates the greatest strategic and economic advantage.

Taken together, the two frameworks describe the same transition from different perspectives. The Infrastructure Maturity Curve explains organizational evolution. The Spend Curve explains the economic consequences that emerge as that evolution unfolds.

From cost optimization to strategic control

The infrastructure maturity point is often viewed through a financial lens. Organizations arrive there because cloud spending has become significant, workloads have stabilized, and the economics of ownership begin to look increasingly attractive.

But cost is only part of the story.

As infrastructure matures, ownership creates advantages that extend beyond economics. Organizations gain greater control over performance, capacity planning, technology roadmaps, and vendor relationships. Decisions become less dependent on external pricing models and platform priorities, and more aligned with the needs of the business itself.

This shift is becoming increasingly important as AI infrastructure economics, regulatory requirements, data sovereignty concerns, and vendor concentration risks become strategic considerations for technology leaders. Infrastructure is no longer simply a utility to consume. For many organizations, it is becoming a capability that directly influences competitiveness, agility, and long-term resilience.

This is why the Infrastructure Maturity Point shown in the framework represents more than a financial crossover. It marks a transition from optimizing infrastructure costs to exercising greater strategic control over the systems that power the business.

The cost of mistiming

The crossover, or inflection point, is a window, not a moment. Organizations that cross it too early or too late both pay, in mirror-image ways. The two failure modes are symmetric.

Move too early and the organization sacrifices the elasticity that fueled its growth. It commits capital and operational complexity before its workloads are stable enough to justify it. The result is overprovisioned hardware, underutilized capacity, and a platform team distracted by infrastructure operations they were not yet ready to run.

Move too late and the organization pays a compounding premium. Cloud spend grows faster than revenue. Architectural decisions become harder to reverse as more services are built on hyperscaler-specific APIs and lock-in deepens. The longer the delay, the larger the migration project becomes. The larger the project becomes, the harder it is to ever justify starting.

Both failure modes compound over multi-year horizons rather than quarters. The earlier organizations evaluate their infrastructure options, the more freedom they have to make deliberate decisions rather than reacting to rising costs, vendor lock-in, or long-term commitments that no longer align with business needs.

Signals you’re approaching the inflection point

How does an IT executive recognize the approach of the maturity point in their own organization? A handful of concrete signals, none decisive on its own, but together describing an organization standing at Stage 4:

- Monthly cloud spend has become large enough to justify a dedicated FinOps or cost-management function.

- The growth rate of cloud spend consistently exceeds the growth rate of revenue or workload demand.

- Workloads are stable: utilization is predictable, peak-to-average ratios are reasonable, surprise events are rare.

- Strategic requirements around data residency, sovereignty, regulatory compliance, or vendor concentration risk are becoming explicit board-level concerns.

- The architecture team is increasingly producing cost-driven design documents — calls to optimize, refactor, or rearchitect for cost rather than for capability.

Why the case for infrastructure ownership is sharper in 2026

Recognizing the inflection point is only part of the challenge. The second question is why this decision appears to be arriving earlier and more forcefully for many organizations than it did a decade ago. Several developments are converging right now to compress the window in which IT leaders can afford to ignore the call.

Public cloud spend is harder to control than ever.

The FinOps Foundation’s State of FinOps 2025 report, covering organizations responsible for roughly $69 billion in public cloud spend, found that workload optimization and waste reduction remain the top FinOps priorities year after year. A parallel Harness analysis estimated enterprises waste roughly 21% of cloud infrastructure budgets, totaling around $44.5 billion across the surveyed population. AI workloads, now in scope for 98% of surveyed FinOps practices, are making the visibility problem worse, not better.

The Broadcom acquisition of VMware has rewritten the lock-in math.

Since November 2023, Broadcom has eliminated perpetual VMware licensing, consolidated thousands of products into four bundles, and forced subscription-only contracts. Reported customer price increases range from 150% to over 1,000%, with AT&T disclosing a quoted 1,050% increase in court filings. Industry surveys suggest roughly half of VMware customers are now actively evaluating alternatives.

Repatriation has moved from theory to practice.

GEICO is repatriating workloads onto a private cloud built on OpenStack and Kubernetes after its public cloud costs ran roughly 2.5x what was projected. 37signals exited AWS and projects savings of $10 million-plus over five years. Dropbox saved around $75 million in two years by building its own infrastructure. The Barclays Q4 2024 CIO survey found 86% of CIOs plan to move some workloads back from public cloud. That is the highest figure the survey has ever recorded.

Hardware costs are rising in ways that compound the cloud cost story.

AI infrastructure demand has drained supply for commodity DRAM, NAND, and server CPUs. Some analysts project DDR5 server modules to double in price by the end of 2026. The five largest hyperscalers are projected to spend $700-725 billion on infrastructure in 2026 alone, buying up the supply at the wholesale level. Those input costs flow through to cloud list prices on a 3-6 month lag.

Together, these developments describe an unusual and volatile market where delaying the infrastructure decision has an additional and sometimes unrecoverable cost attached to it.

Where OpenMetal fits — and what sets us apart

The above framework helps organizations determine whether they are approaching the infrastructure maturity point. Once that determination has been made, the question becomes practical: what does an infrastructure model look like that delivers the predictability, control, performance, and flexibility the framework describes?

OpenMetal’s hosted private cloud platform is built on open-source infrastructure: OpenStack for compute orchestration, Ceph for storage, on dedicated bare metal hardware.

“Most of the clients we see at the inflection point are working toward control over their performance, costs, and their roadmap priority. That impacts how you think about cloud and compute infrastructure as well as every piece necessary for the optimal technical stack.”

Yuriy Shyyan, Director of Cloud System Architecture @OpenMetal

Capacity-based pricing, not consumption-based billing

When you deploy a cloud with OpenMetal, you commit to capacity: fixed compute, fixed storage, predictable monthly cost. There are no surprise egress fees, no per-API-call charges, no metered components that make the bill arithmetic impossible to forecast. For workloads that have moved past Stage 3 stability, this is the structural change that flattens the spend curve in the diagram above.

Dedicated bare metal, not shared virtualization

Your cloud runs on hardware that is yours alone. No noisy neighbors, no shared performance ceiling. For data-heavy, performance-sensitive, or compliance-bound workloads, dedicated infrastructure is not a nice-to-have. It is the architectural difference between predictable performance and best-effort performance.

Open source, not proprietary lock-in

OpenStack and Ceph are the open-source standards underlying much of the private cloud world, including the infrastructure GEICO is repatriating onto. Skills are portable. APIs are stable. The exit cost from OpenMetal is fundamentally different from the exit cost from a proprietary hyperscaler or a single-vendor virtualization platform. In a year that has demonstrated what proprietary platforms are willing to charge for stickiness, that exit option has measurable value.

Operated as a service, not handed to your team

Running OpenStack at production scale is non-trivial; one of the reasons organizations hesitate at the maturity point is the operational lift of owning their own cloud. OpenMetal can assist with operating the platform: hardware provisioning, OpenStack management, Ceph storage, networking, monitoring. The customer’s team gets cloud capabilities; OpenMetal handles the cloud underneath them. The capability-to-operate signal in the framework above stops being a blocker.

Hybrid by design, not by accident

Mature infrastructure is portfolio-managed across environments, and OpenMetal is built to be one node in that portfolio, not the entire answer. The same architecture that gives you elastic public cloud for variable workloads gives you OpenMetal capacity for steady-state workloads. The two coexist, deliberately.

The strategic reframe

The framework here is not an argument against public cloud. Public cloud earns its place in every mature infrastructure portfolio. Elastic workloads, geographically distributed services, managed AI services, and genuinely unpredictable demand profiles all belong there.

The argument is that mature infrastructure is hybrid by design, and that the design decision is made by the leadership team on its own timeline, not imposed by a runaway cloud bill, the Broadcom invoice, or a memory-pricing surge.

At the maturity point, infrastructure ownership stops being a cost center to be optimized and becomes a strategic asset to be deployed. What matters in that role is different from what mattered before it: predictability of cost, control of the stack, sovereignty over data and execution, flexibility to negotiate with multiple providers from a position of strength rather than dependency.

The companies that recognize the inflection point early, and act on it deliberately, define the next decade of their infrastructure strategy from a position of strategic control. The companies that recognize it late do so from a position of constraint, while their cost inputs continue rising on schedules they do not set.

The Infrastructure Maturity Curve is ultimately a decision framework. Every organization moves through the stages differently, but the underlying transition is remarkably consistent: infrastructure evolves from a tool for experimentation into a strategic asset.

The question for every IT executive at scale is not whether the inflection point exists, but whether their organization is approaching it, sitting on it, or already past it—and what infrastructure decisions will follow. The companies that recognize that transition early gain the freedom to shape their economics, architecture, and roadmap on their own terms.

Where does your organization sit on the curve? If the signals in this framework sound familiar, the next infrastructure decision is worth a deliberate conversation. OpenMetal helps engineering and infrastructure leaders evaluate whether — and when — a shift toward hosted private cloud makes economic and strategic sense for their workloads.

More from the Runway Intelligence Series

Citations and References:

- FinOps Foundation. State of FinOps Report 2025. State of FinOps Report 2025

- Harness. FinOps in Focus 2025. Harness FinOps in Focus 2025

- Ars Technica. Broadcom proposed 1,050% VMware price hike, AT&T says. Ars Technica Article

- FinOps Foundation. State of FinOps 2026. State of FinOps 2026

- Futuriom. GEICO Shows the Way to Repatriation. Futuriom Article

- 37signals. Leaving the Cloud. 37signals Blog